If Telo Were a Chinese Startup: Industrial Velocity and Automotive Hegemony

The contemporary automotive landscape is characterized by a stark divergence in industrial velocity, primarily driven by a fundamental shift in the geography of innovation. Telo Trucks, a Silicon Valley-based startup developing the MT1—a highly compact, 500-horsepower electric pickup—serves as a quintessential case study in Western architectural brilliance constrained by structural inertia. While the Telo MT1 offers a radical reimagining of the American utility vehicle, compressing the capabilities of a mid-size truck into the footprint of a Mini Cooper, its journey from prototype to production is currently ensnared in the standard multi-year development cycles of the North American manufacturing sector. If Telo were a Chinese company, the MT1 would likely be in mass production by 2026, supported by a state-coordinated financing model, a geographically dense supply chain, and an industrial culture that treats hardware with the iterative speed of software.

The Telo MT1: Architectural Innovation and the American Bottleneck

The Telo MT1 is a design-led response to the increasing “bloat” of the American pickup truck. Measuring exactly 152 inches in length, the vehicle challenges the cultural dictum that bigger is necessarily better. Despite its diminutive size, the MT1 features a five-passenger crew cab and a five-foot bed, achieved by eliminating the traditional internal combustion engine hood and utilizing a wheel-at-each-corner design. Its performance metrics—500 hp, a four-second zero-to-60 mph time, and 350 miles of range—place it in direct competition with premium electric trucks like the Rivian R1T or the Ford F-150 Lightning, but at a significantly lower projected base price of approximately $41,520.

However, the production timeline for Telo reflects the precarious nature of Western hardware startups. Founded in 2023, the company has raised approximately $27 million across its seed and Series A rounds. In the United States, such funding is sufficient for prototyping and low-volume vehicle building via partners, but it remains a fraction of the capital required for high-volume manufacturing. Consequently, while Telo has unveiled functional pre-production trucks and is undergoing final crash certification, mass retail availability is not expected until 2027. This timeline—spanning four to five years from conceptualization to mass delivery—is the “Western standard,” a pace that increasingly appears sclerotic when compared to the industrial benchmarks established in the Chinese new energy vehicle (NEV) sector.

The “China Speed” Phenomenon: Xiaomi as the Counter-Fact

The hypothesis that Telo would be in production by now if it were Chinese is best supported by the trajectory of Xiaomi Auto. Xiaomi, a consumer electronics giant, announced its entry into the EV market in March 2021. By December 2023, the company had not only designed the SU7 sedan but had completed its first-phase factory in Beijing. Official deliveries began in March 2024, and by the end of that year, Xiaomi had delivered 140,000 units. This represents a transition from zero automotive footprint to mass-volume manufacturer in approximately 36 months—a feat that Telo and other U.S. startups have struggled to replicate due to fragmented funding and regulatory friction.

Xiaomi’s success is a product of what industrial analysts call “China Speed.” This phenomenon is driven by a competitive industrial architecture where Chinese EV firms typically take 20 months to develop a new car, compared to 40 months for Chinese legacy automakers and up to 60 months for Western firms. By early 2026, Xiaomi had already delivered over 381,000 first-generation SU7s and was preparing to launch a refreshed model with upgraded LiDAR and smart driving hardware. If Telo were operating in this environment, it would have leveraged existing platform architectures and a pre-certified supply chain to compress its validation and ramp phases significantly.

The Geographic Imperative: The 4-Hour Industrial Circle

A primary catalyst for production speed in China is the “4-hour industrial circle” located in the Yangtze River Delta. This region, including hubs like Shanghai, Suzhou, and Hefei, has coordinated its industrial clusters so that an NEV factory can source approximately 80% of its critical components—batteries, motors, chips, and services—within a four-hour drive. This geographic agglomeration minimizes logistics bottlenecks and allows for “interlocking innovation flywheels,” where advances in one sector, such as automotive semiconductors, rapidly catalyze breakthroughs in another, such as autonomous driving software.

In Suzhou alone, over 600 companies form an intelligent vehicle-centered industrial chain. This density allows startups to prototype and iterate with unprecedented velocity. For Telo, which must navigate a fragmented U.S. supply chain where battery cells, aluminum panels, and specialized motors may be sourced from different states or even different continents, the lack of such a concentrated cluster is a structural disadvantage that extends lead times and inflates costs.

The Financing Chasm: Hefei’s Master Strategists vs. U.S. Venture Volatility

The divergent fates of EV startups are often determined by the philosophy of their capital providers. In the United States, startups like Telo, Canoo, and Rivian rely on venture capital and public equity markets. This capital is notoriously volatile and sensitive to interest rates, as evidenced by the January 2025 Chapter 7 bankruptcy filing of Canoo. Despite raising over $1.41 billion in total funding and securing major orders from fleet operators, Canoo succumbed to a heavy loss in cash and a failure to secure emergency funding.

In contrast, the “Hefei Model” in China represents a paradigm shift where local governments act as professional venture capitalists. When NIO faced a delisting crisis and a net loss of 11.4 billion yuan in 2019, the Hefei government provided a 7-billion-yuan anchor investment. This was not a blind subsidy but a “scientific judgment” based on exhaustive due diligence of NIO’s patents and battery-swapping efficiency. In return, NIO established its headquarters in Hefei, acting as a magnet for battery giants and chipmakers. By 2025, Anhui province had become the top region in China for total vehicle production and NEV output.

If Telo were a Chinese company, it would not be scrounging for a small Series A; it would be receiving multi-billion-yuan lifelines from a municipal government that views Telo’s success as vital to the city’s ecological niche in the smart utility sector.

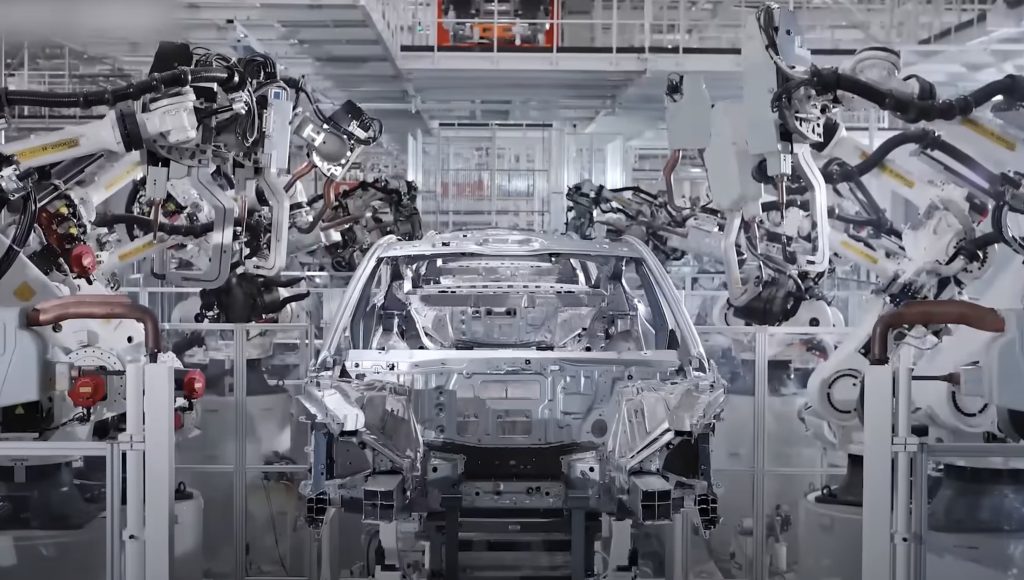

Manufacturing Paradigms: Gigacasting and Vertical Integration

The production of the Telo MT1 would also be accelerated by the massive adoption of gigacasting technology in China. Originally introduced by Tesla, gigacasting—the process of forming large body parts from a single cast—has taken China’s car factories by storm. By 2025, 80% of all gigacasting machines on Earth were installed in China. Xiaomi’s Beijing factory uses a 10,000-short-ton press to replace 72 separate parts with a single gigacast part, saving half the production time required for conventional assembly.

Furthermore, Chinese OEMs benefit from a fundamentally lower cost structure driven by extreme vertical integration. BYD, the market leader, produces 80% of its Tier 1 components in-house, eliminating supplier markups and providing a significant per-vehicle advantage over competitors. Additionally, Chinese firms utilize aggressive supplier-backed financing, with payment terms extending up to 225 days, compared to the 60-day standard for many Western firms. This effectively provides zero-interest capital to fund production ramps.

Regulatory Friction and the Administrative Veto

The U.S. regulatory environment acts as a significant “time tax” on production. Rivian’s experience in Georgia illustrates this: despite announcing its $5 billion plant in 2021, construction was delayed for years by citizen lawsuits and zoning disputes. Litigation expenses were immense as the state fought to overcome attempts to stop the plant. Vertical construction is only slated to begin in 2026, with customer vehicle production not anticipated until 2028.

In contrast, China manages a streamlined “Catalog” approval system. While regulations are strict, the “visible hand” of policy works in tandem with the market to solve administrative bottlenecks. The “industrial chain leader system” ensures that high-ranking government officials directly address site acquisition and licensing issues. If Telo were Chinese, its model approval would be a matter of months, and its factory site would be secured through a “flash marriage” between the state and the startup, similar to the 65-day deal between Hefei and NIO.

Market Viability and the Mini-Truck Segment

The Telo MT1 occupies a unique niche in the U.S. light commercial vehicle market, which remains heavily dominated by traditional internal combustion engines. In China, however, the mini-truck market is driven by rapid urbanization and an explosion in last-mile delivery services. This segment is projected to grow at a 15% CAGR, favoring compact, maneuverable electric vehicles.

Telo’s MT1, if produced in China, would be a premium entry in a high-volume “blue ocean” market rather than a niche vehicle in a Western market struggling with adoption plateaus. While U.S. protectionism shields startups from cheap imports, it also isolates them from the advanced and mature supply chains required to scale quickly.

If Telo were a Chinese company, it would be operating within an ecosystem where innovation follows manufacturing. It would have had its gigacasting dies cut in late 2023, its regulatory entry approved in early 2024, and its first 100,000 units delivered by mid-2025. In the United States, the Telo MT1 remains a brilliant Silicon Valley creation, but its production status in 2026 is a sobering reminder of the geographic disparity in industrial power. The future of American niche automakers depends on whether the West can build its own versions of industrial clusters and coordinated financing to match the velocity of the global automotive hegemon.